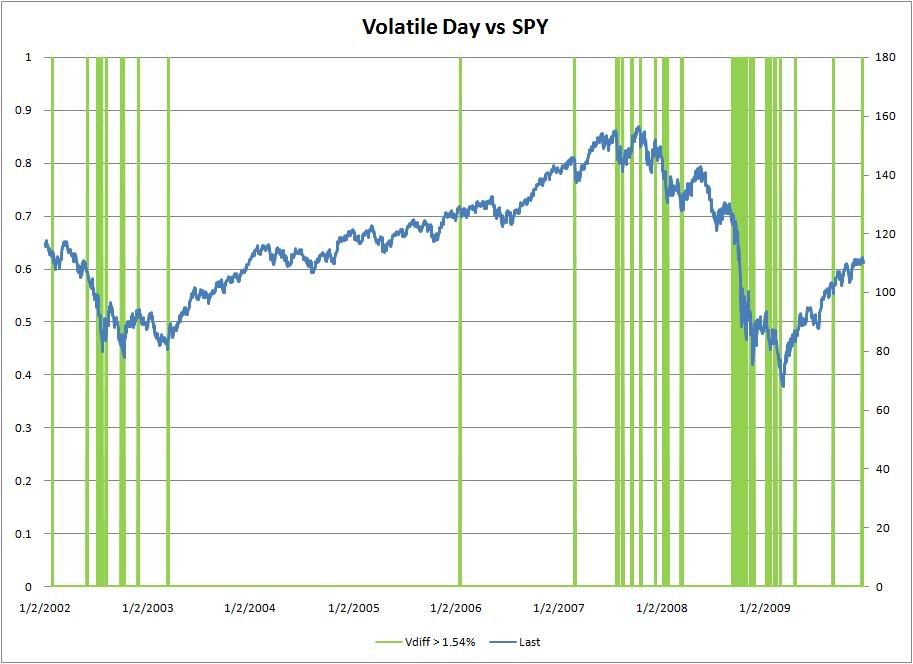

I first check if there’s any follow through on up and down day with daily volatility higher than two standard deviations.

There are 25 instances of up days which have volatility two standard deviation higher than 20 day moving average of volatility (V>V20) out of 2007 days since 2002. Out of 25 instances, 2 instances occurred in January 2007, 5 instances are from July 2002 to October 2002, 12 instances are from September 2008 to February 2009 which coincides with the steepest drop in recent market history. My take on this phenomenon is that once market becomes hectic, the madness will continue for a while. A true longer term bottom will not be put in on a day of huge rally; extreme up days are rare in a market that’s truly going up. On days with high volatility, 52% is followed by up day. The number is really too low to provide any useful information.

The above chart show volatile up days and SPY daily close price plotted on the same chart. From the chart, it is very clear that in recent market history volatile days (even up days) are associated with weak market.

There are 32 instances of down days which have volatility two standard deviations away from the V20 in the negative side. Out of the 32 instances, 2 instances are from July 2002, 6 instances in second half of 2007, and 19 instances are from September 2008 to April 2009. The extreme negative data also supports the hypothesis that days deviate from the volatility means tend to appear near each other. Out of the 32 instances, 56.2% closed higher than the next day. Once again, the number is really too low be of any significance. However, this finding does confirm with earlier hypothesis that extreme weakness tends to be followed by short term bounce rather than more immediate weakness.

I split data into tow group of V20>2%, and V20>1%, but doing so have not yield much useful data so far.